2025 Full-Year Iron Ore Market Review

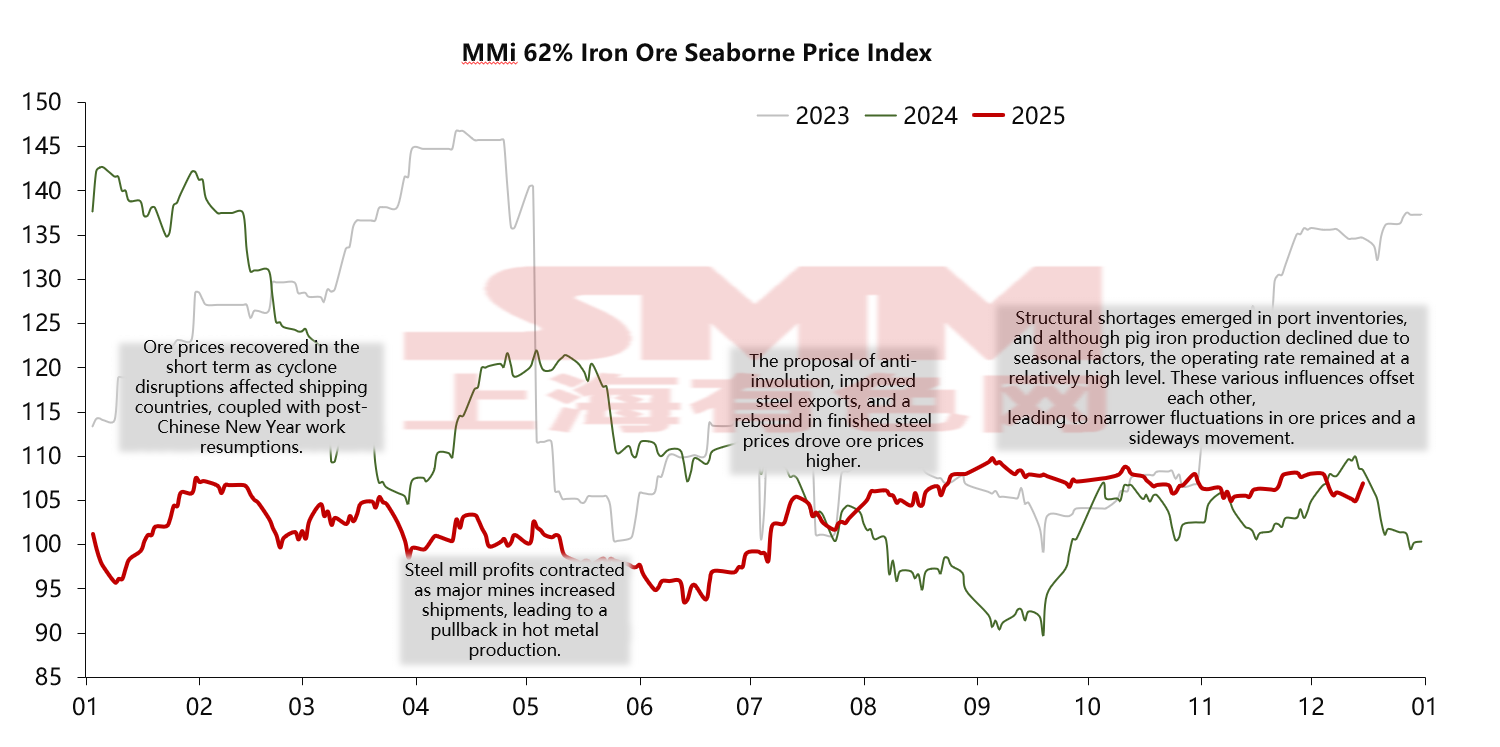

The iron ore market in 2025 did not experience the widespread collapse predicted by some pessimistic forecasts. Instead, it followed an "N-shaped" trend characterized by "higher lows and capped highs." Overall, the price volatility of iron ore in 2025 was significantly narrower compared to the previous two years.

Beginning of the Year (Q1)

Market sentiment was buoyed by expectations stemming from the 2024 Central Economic Work Conference and the anticipated issuance of a trillion-yuan in special treasury bonds. Concurrently, supply from major producers, Australia and Brazil, faced more frequent cyclones and rainy season disruptions than in previous years, leading to a short-term drop in iron ore shipments and arrivals at ports. This tightening of the supply-demand balance briefly drove prices higher, peaking around $107/tonne. However, the post-Chinese New Year resumption of work and production was sluggish, and the recovery in hot metal output lagged behind expectations, causing prices to start correcting from March.

Second Quarter (Q2)

Iron ore prices generally trended downwards, hitting their lowest point of the year in late June, briefly breaking the $100/tonne psychological barrier and bottoming out in the $93–95/tonne range. The primary drivers were the failure of the traditional "Golden March, Silver April" peak season to materialize, coupled with the US imposing additional tariffs, which squeezed finished steel product prices and led to wider losses for steel mills. Hot metal production retreated from its highs, pulling down the prices of steelmaking raw materials.

Third Quarter (Q3)

Iron ore prices began to rebound. Key drivers included: "Anti-involution" measures proposed by China in July, and steel exports hitting a historical high for the same period in August-September. Furthermore, the Chinese government released more proactive economic growth signals, notably financial support for social housing and urban village renovation projects. This significantly reignited expectations for infrastructure spending to prop up the economy in the second half of the year, directly alleviating pressure from insufficient demand in the construction sector and supporting iron ore consumption.

Fourth Quarter (Q4)

Pig iron output saw a seasonal decline, but steel mill operating rates remained relatively high. Some steel mills delayed maintenance schedules, anticipating next year's capacity ceilings, which shifted the usual hot metal output decline later into the year. Additionally, the temporary suspension of Jimbuba fines from being cleared from ports, combined with persistently high demand for medium-grade fines, led to a structural shortage in port inventories. However, the market was simultaneously filled with negative speculation regarding the Simandou iron ore project and concerns over a massive supply release next year. These countervailing factors offset each other, narrowing price volatility, and keeping iron ore prices oscillating in a range best described as "unable to fall, but also unable to rise."-----2026 and Future Iron Ore Market OutlookGlobal Iron Ore Supply-Side Changes

Source: SMM

2026 and Future Iron Ore Market Outlook

Global Iron Ore Supply-Side Changes

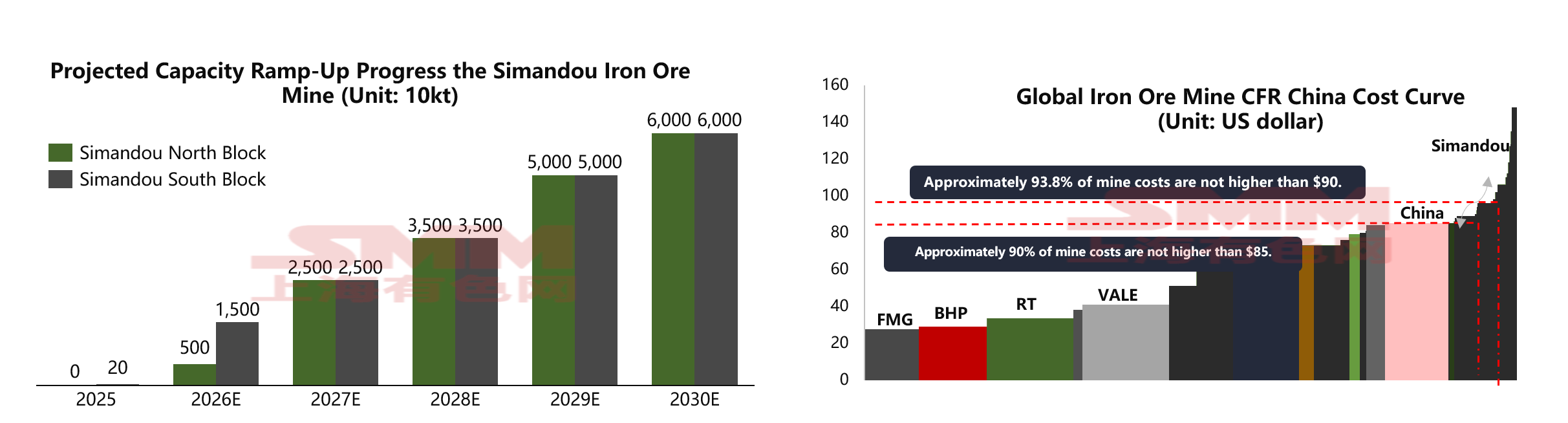

Based on our tracking of global iron ore projects, six new large-scale projects are expected to commence production in 2026, including the northern section of the Simandou iron ore project and Vale's Northern System expansion. When factoring in the Simandou southern section, which started production at the end of this year, and the output ramp-up from other previously commissioned projects, nearly 60 million tonnes of new iron ore capacity are projected to hit the market next year, with the majority concentrated in the first half. Consequently, short-term capacity pressure will continue to suppress iron ore price upside.

Source: SMM

Regarding the Simandou project, while its total 120 million tonnes of production capacity is well-known, its impact on the market will be gradual. According to Rio Tinto's 2026 production guidance, the Simandou South block is expected to yield 5 to 10 million tonnes in 2026. Combined with the development progress of the Winning Consortium Simandou (WCS), the entire Simandou project's export volume is projected to be between 20 and 30 million tonnes in 2026. From a freight cost perspective, the northern section is expected to have a cost advantage over the already commissioned southern section. The initial shipping cost for the South block will be relatively high, around $137/tonne, due to high financing costs. However, as output ramps up, the cost per tonne is expected to gradually drop to about $67. Overall, the average cost for both the North and South blocks of Simandou is projected to gradually decrease from $100/tonne in 2026 to around $64/tonne by 2028. This suggests that by around 2028, Simandou will become one of the world's lowest-cost mines, with production expected to reach approximately 60 million tonnes by then, still leaving about half of its full capacity to be realized. Other projects are also slated for commissioning in the following two years.

Source: SMM

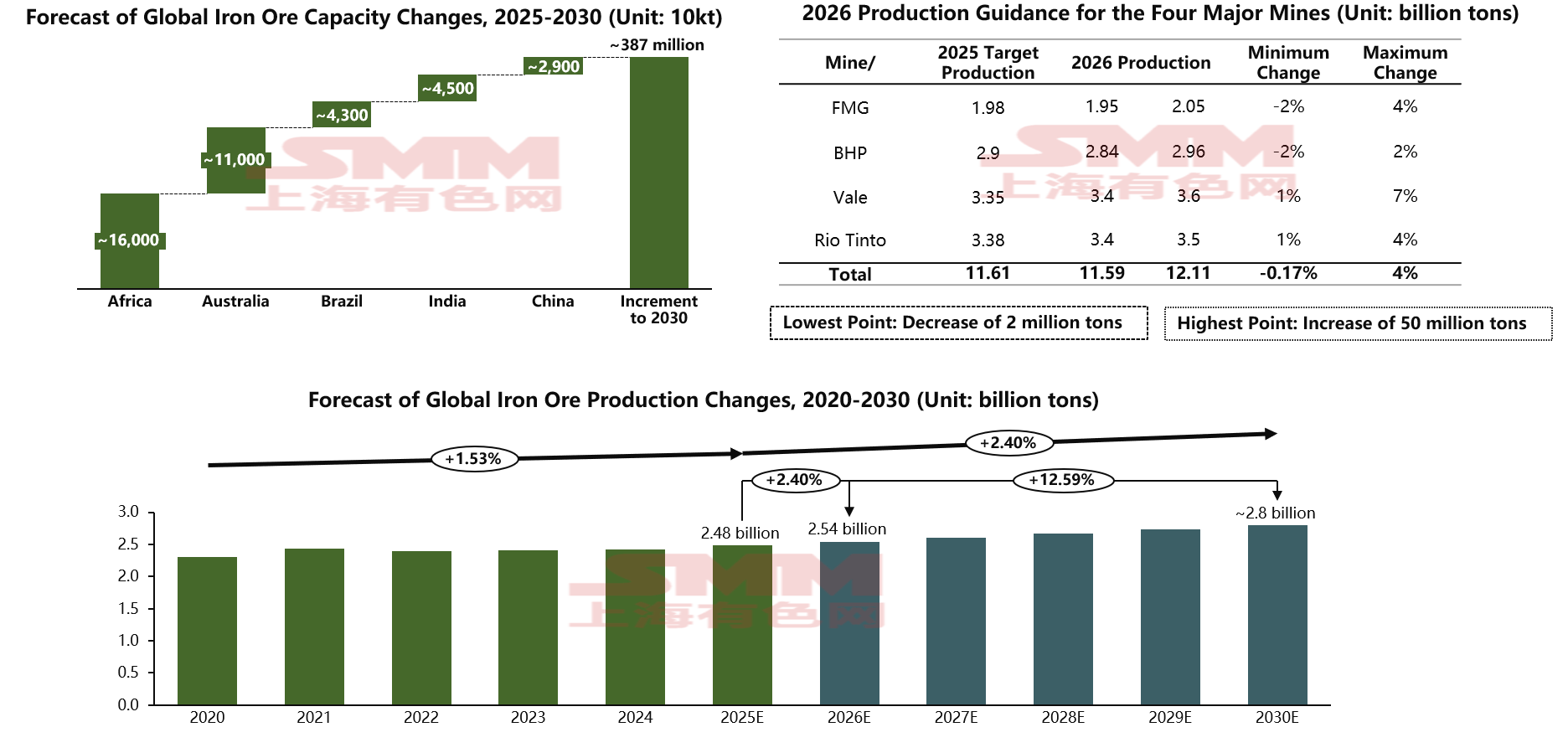

Forecasting conservatively to 2030, the global iron ore capacity increment is projected to be close to 380 million tonnes entering the market. While increases from China and India will primarily supply their domestic markets, a significant portion of the new capacity from Africa, Australia, and Brazil will be exported into the seaborne market, posing a challenge to iron ore prices. Although capacity is not perfectly equal to output, future production will not be substantially lower than capacity. Regarding the output from the four major miners (the "Big Four"), their iron ore release is anticipated to increase by up to 50 million tonnes in 2026 compared to this year. Including ramp-ups from non-mainstream miners, the global iron ore supply in 2026 is forecast to reach approximately 2.54 billion tonnes, a year-on-year increase of about 2.4%. By 2030, if all projects proceed smoothly, global iron ore supply is expected to reach approximately 2.8 billion tonnes. Collectively, both capacity and output are poised for substantial growth starting from 2026, while demand is highly unlikely to keep pace with the expansion in supply.

Source: SMM

Global Iron Ore Demand Shift

The global flow of iron ore is also projected to change significantly in the coming years. As China begins to encourage domestic steel mills to develop overseas markets and restructures its domestic industrial chain to produce high-end finished steel products needed for the manufacturing sector, a large volume of high-polluting, low-value-added, low-end capacity is set to be eliminated in China. Consequently, China's demand for iron ore is expected to decrease year by year.

Starting in 2026, China's crude steel output is projected to experience a slight decline, followed by a more noticeable drop from 2028 as backward capacity is retired, ultimately reaching an estimated 950 million tonnes by 2030. Concurrently, India is set to emerge as a new growth engine for the steel industry, driven by infrastructure and real estate, achieving rapid expansion with an astonishing projected average annual growth rate of 10.5%. India's crude steel output is expected to reach 167 million tonnes in 2026 and 200 million tonnes by 2030. Beyond India, the steel industry in Southeast Asia is also developing rapidly, with countries including Vietnam and Indonesia projected to rise quickly at a compound annual growth rate exceeding 5% over the next five years. The total crude steel output in Southeast Asia is forecast to reach approximately 75 million tonnes next year and 100 million tonnes by 2030. However, against the backdrop of declining Chinese crude steel output and global carbon reduction efforts, the most direct impact on iron ore is a slow growth in demand. Considering the crude steel output and iron ore demand from several major countries, global iron ore demand is only expected to increase by just over 20 million tonnes in 2026, which clearly falls short of the estimated supply increase of around 70 million tonnes.

Source: SMM

Furthermore, from a long-term demand structure perspective, the share of Electric Arc Furnace (EAF) steelmaking and Direct Reduced Iron (DRI) in global crude steel production is slowly increasing. Despite the current high-speed development of crude steel output in emerging markets (excluding China), given that China remains the largest blast furnace steelmaking nation—with its production scale nearly ten times that of the second-largest producer, India—and that some overseas new capacity is EAF-based, the total global iron ore demand still faces downside risks as China's crude steel output plateaus or declines.

Supply-Demand Balance and Iron Ore Price Center Forecast

According to SMM's forecast, the global iron ore supply-demand surplus is projected to widen to approximately 190 million tonnes in 2026 due to the commissioning of large projects and moderate overseas demand growth, representing a year-on-year increase of over 40 million tonnes. This supply pressure is expected to suppress the average annual price, which may settle around $98/tonne. In the long term, 2028 may be a critical juncture. If the average price falls below $90/tonne, some high-cost, non-mainstream mines may exit the market, thereby alleviating the surplus pressure and further increasing global supply concentration. Following this, the iron ore price is expected to enter a new equilibrium range around $90/tonne.

Source: SMM

![[SMM Daily Hot-Rolled Coil Trading] Spot Trading Continued to Fluctuate](https://imgqn.smm.cn/usercenter/rBCZR20251217171716.jpg)